Living in California you’re well aware of the threat of quake damage, even if you don’t live near the most notorious fault lines. Yet you might not know that in order to be covered for damage from an earthquake you’ll need to purchase a separate earthquake insurance policy as a companion to your homeowners policy.

- Quake coverage isn’t included by default with homeowners policies, but your carrier is required to offer you an option to purchase each year.

- In California over 1.5 million households carry quake insurance and the California Earthquake Authority (CEA) is the most popular choice.

- The average policyholder in California pays about $120 a month for $800,000 in coverage. That can be higher or lower based on factors like the earthquake risk of your location, characteristics of your home like foundation type, age, and number of stories, as well as the deductible and coverage you choose.

What does quake insurance cover?

The base dwelling coverage of an earthquake policy covers damage to your home caused directly by an earthquake, including:

- Foundation cracks

- Structural damage to walls, ceilings, and floors

- Damage to chimneys, though typically with capped limits

- Damage to stucco walls and with some policies exterior masonry

- Damage to walkways and patios required to enter your home

- Damage from landslides immediately triggered by the quake

It does not typically cover:

- Flood damage caused by a tsunami triggered by the earthquake (flood insurance can cover this)

- Fire damage (your homeowners insurance typically covers this)

- Damage to the soil or land your home sits on, except for limited amounts to stabilize the soil

- Damage to landscaping

Not always included but available (sometimes for an extra premium):

- Loss of use. You can also pay extra for ‘loss of use’ coverage to handle the cost of renting temporary housing while your home is being repaired.

- Other structures. The CEA automatically includes coverage for detached garages and structures, but won’t cover pools and spas. Other carriers only cover detached structures for an extra premium, but will also allow coverage for pools.

- Personal contents. Damage to items inside your home can also be covered for an extra premium.

Your homeowners policy won’t cover any of these expenses from an earthquake unless you add a companion earthquake policy.

What about FEMA?

- FEMA grants for home repairs max out at $43,500 and federal disaster loans cap out at $500,000. We run through FEMA scenarios in detail here.

- We estimate a modest 2,500 square foot home can expect $250,000 – $800,000 in damage following severe shaking based on a UC Berkeley analysis detailed below.

- Repairs can take months to years in some cases, and FEMA grants for temporary housing also max out at $43,500.

A quake insurance policy can help you avoid dipping into your investments or taking on what amounts to the payments on a second mortgage via an SBA disaster loan.

What deductible to choose?

Earthquake insurance deductibles are typically stated in a percent of the coverage amount like 10% instead of a round dollar amount like $10,000.

Over half of California homeowners insured by the California Earthquake Authority (CEA) in 2022 opted for a 15% deductible, translating to a $120,000 deductible for an $800,000 policy.

Deductible Options and Considerations:

- The CEA offers deductibles ranging from 5% to 25%. Other insurers like GeoVera and Palomar offer lower options, as low as 2.5%. Lower deductibles equate to higher premiums.

- On an $800,000 home, the deductible would be:

- 2.5%: $20,000

- 5%: $40,000

- 10%: $80,000

- 15%: $120,000

- 20%: $160,000

- You don’t pay the deductible to the insurance company. The insurance company pays for the repair cost minus the deductible amount.

Factors to Determine Your Affordable Deductible:

- Emergency Savings: A higher deductible is feasible if you have a substantial emergency fund to cover the deductible and initial recovery costs including temporary housing.

- FEMA assistance. You might also qualify for federal assistance after a major quake which can sometimes be used to cover the shortfall a deductible creates, though the federal estimate for damage might be lower than your estimate because FEMA only looks at the cost to return a home to basic living standards. Your insurance will look at the cost to return your home to its prior standard.

- There’s a maximum FEMA grant of $43,500 for repairs, though it’s rare to receive the maximum grant. For temporary housing while your home is repaired the maximum is a separate $43,500.

- Federal disaster loans. These are available with rates and terms similar to a mortgage, though with rate discounts for those who don’t qualify for market mortgages. The max loan amount is $500,000 and like a mortgage must be repaid or you can lose your home.

How much does earthquake damage cost?

When figuring the coverage and deductible of a quake policy you’ll want to have an informed conversation with a licensed insurance agent.

To help with that discussion we reviewed a 2019 UC Berkeley study that conducted a simulation of earthquake damage of common home types in California based on 4 historic quakes (including Northridge, a 7.0 in San Francisco, a 6.8 in San Bernardino, and 6.5 in Bakersfield). The study had insurance adjusters estimate the cost to repair various damage states that occurred in the simulation.

Based on data from that study and assuming a basic 2,500 square foot tract home, we estimate the following earthquake repair costs depending on the severity of damage from cosmetic to full replacement:

- Cosmetic damage: $21,875 – $46,875

- Significant finish damage (drywall, chimney), no structural damage: $53,125 – $106,250

- Replace interior and exterior finishes (drywall, siding, chimney): $250,000 – $331,250

- Replace entire structure: $625,000 – $743,750

How did we get those figures?

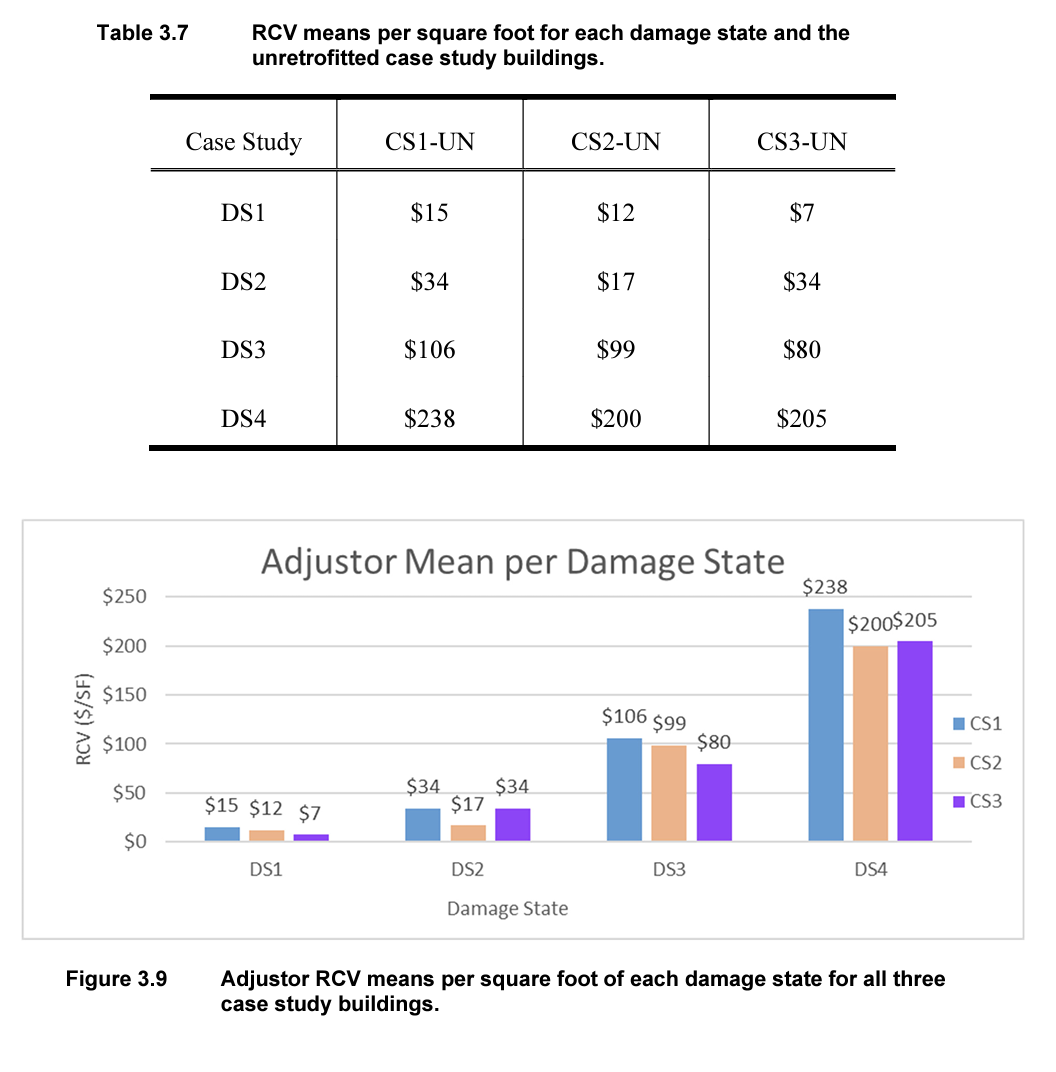

The Berkeley study estimated repair costs in 2019 dollars per square foot were:

- Cosmetic damage: $7-$15 / square foot

- Significant finish damage, no structural damage: $17-$34

- Replace interior and exterior finishes (drywall, siding, chimney), some structural damage: $80-$106

- Replace entire structure: $200-$238

Assuming a 25% increase in costs to consider inflation since 2019, more modern finishes, and the possibility of a surge in costs after a large quake, we estimate repair costs of:

- Cosmetic damage: $9-$19 / square foot

- Significant finish damage, no structural damage: $21-$42

- Replace interior and exterior finishes (drywall, siding, chimney): $100-$132

- Replace entire structure: $250-$298

We then multiplied those square foot costs by 2,500 square feet to get the damage repair estimates.

You can use the square footage of your home to get a rough estimate and have a conversation with a licensed insurance agent. Homes with more luxurious finishes or complex construction can expect higher repair costs.

And looking at real world examples…

- The magnitude 6.0 2014 Napa earthquake caused an estimated $1 billion in damage, with individual repairs ranging from $10,000 to $500,000 or more.

- The 2018 Anchorage earthquake even saw newer homes with damage in the hundreds of thousands of dollars owing to varying construction standards and soil conditions.

- The 1989 Loma Prieta earthquake left two blocks of homes on Eighth Avenue in the Sunset District of San Francisco damaged or destroyed and uninhabitable for months due to a landslide on a relatively small slope, even while homes across the street were completely unscathed. This was far from the destruction in the Marina District.

While retrofitting can’t completely eliminate the chance of having to replace the entire home after a quake, it can have a substantial benefit.

- The Berkeley study found bracing and bolting homes built prior to the 1980s to current standards can reduce the damage estimate by 65% vs a retrofitted home.

- Retrofitting typically costs $3,000 – $10,000.

- You might also receive a significant discount on your earthquake insurance premium

What about aftershocks?

Big earthquakes have aftershocks, some of them big and damaging too. Does that mean your deductible resets each time?

Yes and no.

- The CEA counts a quake and all aftershocks within 360 hours (15 days) as one event with one deductible. Other carriers may have shorter windows.

- A carrier can’t cancel your policy before its renewal because of a quake, but your deductible resets if a quake hits beyond the 360 hour window for a CEA policy, or the applicable window for another policy.

In practice you might find yourself and the carrier debating whether damage from a later aftershock was set up by damage from the earlier quake.

How to shop for quake insurance

A good first step is to get a rough sense of what quake insurance might cost for a home like yours.

Our tool lets you get a quick estimate of CEA and other carrier premium costs with no email or phone number required before you have a conversation with your carrier or agent.

While quake policies have similar basic coverage, they vary in how comprehensive they are. For example CEA won’t cover masonry veneer or breakables like dishes and china, while other carriers might.

- CEA backed quake insurance is only available through your homeowners insurance carrier. Most carriers participate, though some like GEICO do not, and use other options.

- You should also review quotes and coverage from non CEA options like GeoVera or Palomar. They sometimes have lower rates and broader coverage than the CEA. Those are available through any affiliated agent – you don’t need to go through your homeowners carrier and you don’t need to change your homeowners carrier to qualify.